At Multiplicity we create value by providing secondary market liquidity for niche alternative investment funds. Litigation funding is one of these niches that is maturing and where a need for secondary market liquidity is emerging.

A young asset class…

Litigation financing is a fairly modern concept and is still viewed and regulated differently across jurisdictions. In certain jurisdictions – also through codes of conduct of attorneys – lawyers are prohibited from funding legal cases of their clients, and thus, funding of litigation through independent third parties has come up. The modern concept emerged in the UK during the second half of the last century; in the US, the concept has become more accepted later on. Since the turn of the century, litigation financing has become an accepted concept that has been formalized by both the regulator and trade associations.

…is maturing

While the financing of litigation was initially more opportunistic in nature, litigation financing has become more and more institutionalized, with professionally managed litigation funds providing funding over the last twenty years or so.

Litigation financing remains the realm of primarily professional investors. Still, other funders have taken a broader approach – Burford Capital, a global litigation financer, for instance, has even opted to list its entire business on the London AIM stock exchange. As a result, it has received the “AIM Award for Innovative Fundraising of the Year” for it. The undisputed and critical advantage for investors in litigation financing is the distinct nature of investment returns that are completely uncorrelated to the macroeconomic environment and financial markets. Given that institutional pools of money are professionally managed, the manager will also ensure that only cases with a high likelihood of success are funded.

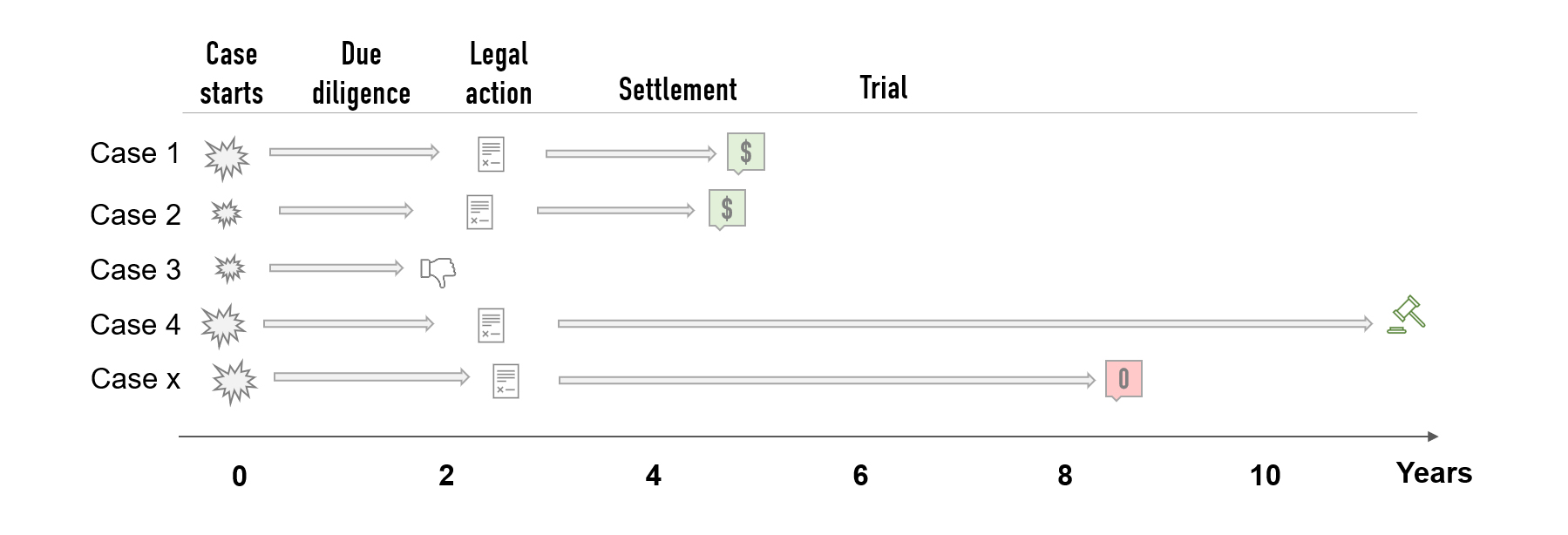

Institutional litigation finance investment funds generally have a life cycle comparable to that of a private equity fund: During the ‘investment period’, new legal cases are added to the fund’s portfolio, followed by a period during which only additional funding to existing cases is added. During this time, successful cases will also pay the fund, and this capital will be returned to investors. Funds generally have a well-defined life span and may be extended in line with the fund’s constitutional documents.

Figure 1: Illustrative life span of a litigation fund

Maturing means learning

A negative side effect of institutional litigation financing through investment funds is that certain legal cases take substantially longer than initially anticipated – in certain cases well beyond the life span originally agreed for a litigation fund. In the worst case, investment funds do not have enough cash available to continue funding long-lasting (but generally promising) legal cases. They have to find additional funding, either from existing or new investors – with the detrimental risk of substantially diluting existing investors’ interests.

Many of these interests are in successful funds that have generated positive returns for investors where monies awarded in successful cases have already been distributed.

Through these distributions, these tail end positions often have become small and irrelevant in the overall success of the fund’s investment. Given the young age of the asset class, there is only a very limited secondary market for such fund interests available at present, particularly interests with an older vintage and a smaller size.

Multiplicity – your provider of liquidity

Multiplicity Partners has successfully emerged as a secondary buyer of illiquid private fund interests, ranging from well-established tail-end private equity, private debt and real estate funds to lesser-known niche strategies such as ILS (Insurance-linked Securities), shipping, or royalty related interests.

Multiplicity Partners is also an active buyer of tail-end litigation fund interests and provides liquidity solutions for investors that may no longer wish to participate in a litigation fund’s ongoing cases. We have come across many tail end litigation funds and have profound insights into pricing and transferring such investments fairly. We have successfully concluded secondary transactions in litigation fund interests and are ready to offer solutions for existing litigation fund investors seeking liquidity.

Would you like to receive a quick indicative pricing for your asset? Or share your views on this article? Please write to Christoph today at cl@mpag.com, or call him at +41 44 500 4410.