We firmly believe that the main focus of independent fund directors should be on risk. Actively managing the “upside” is the job of the investment manager. The directors should focus on what can go wrong.

In a nutshell asset managers should just “say what they do and do what they say”. This means they should clearly explain investors how their money is going to be invested and then stick exactly to their promises. To assure this, the investment portfolio must be managed within a whole range of restrictions and risk limits. The risk oversight function of the fund board should give fund investors assurance that the investment manager does not breach these restrictions.

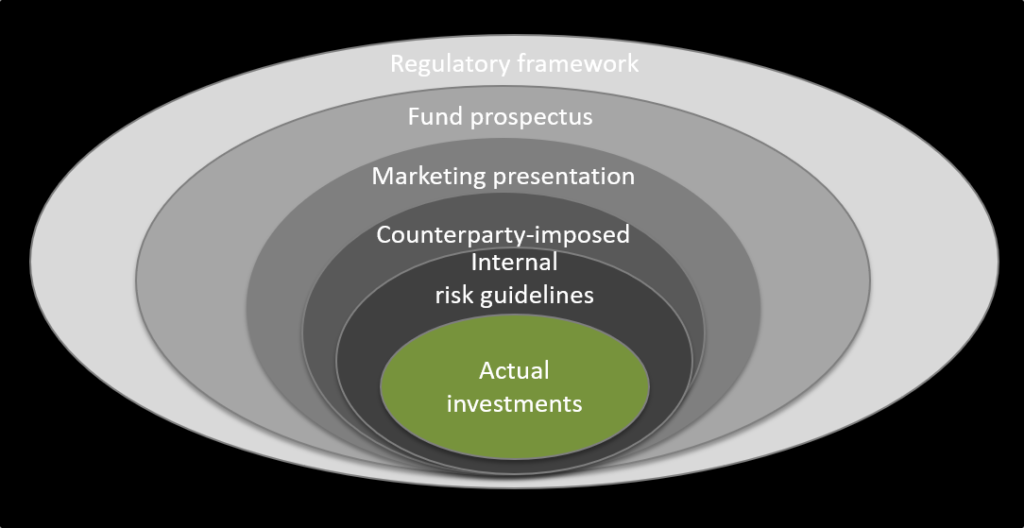

Figure 1: Various levels of restrictions imposed on portfolio management

Let’s now look at these different levels of important limitations in more detail:

- Regulatory framework: Terms and the investment strategy described in the fund prospectus, marketing brochures, KIIDs or also verbally must comply with the relevant regulatory framework. For example, you cannot claim to follow a fixed income arbitrage strategy in a UCITS fund if this would require high degrees of leverage.

- Fund prospectus: The prospectus explains what terms and investment strategy are offered to investors and defines a set of legally binding restrictions, typically much narrower than what is allowed by the regulator. For example, it claims to follow a value-oriented large-cap equity strategy in US markets.

- Marketing presentation: Marketing material such as pitch books, due diligence questionnaires and factsheets typically narrow down the investment flexibility further. For example, fund investors may be told about specific targets for returns, volatility and tracking error.

- Counterparty-imposed: In more complex investment strategies, the investment manager might be further restricted by capital requirements and other limitations dictated by counterparties such as prime brokers or swap counterparties (e.g. in ISDA agreements).

- Internal risk guidelines: Based on all of the above restrictions, the risk manager’s job is to define a clear set of internal risk guidelines that should make it very unlikely to ever break any of the externally binding limits. For example, if the prospectus states that no single equity position will exceed 10% of NAV, then the internal guidelines will set the limit to maybe 8% such that it is highly unlikely to have a passive breach if the stock price exhibits a sudden and sharp increase.

- Actual investments: To avoid to many interferences with risk management, portfolio managers probably do not want to test the boundaries too often and navigate with a safety margin to the internal limits.

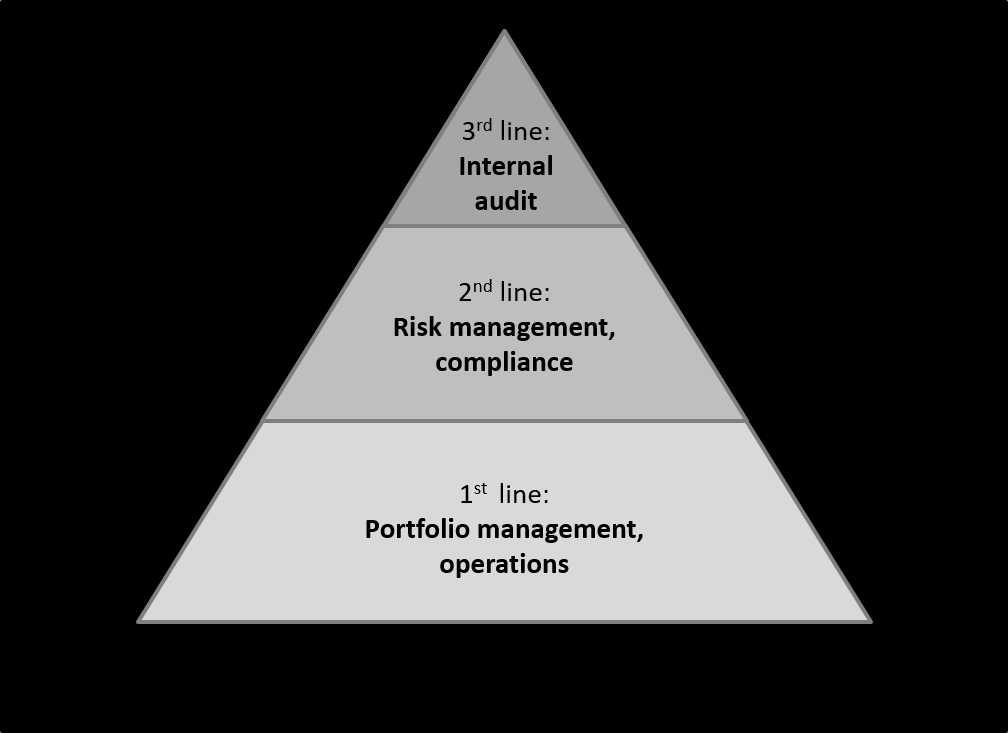

We believe that effective fund governance requires the board to understand these levels of restrictions. Of course, fund directors do not need to manage risks on daily basis but they should be able to judge the reliability of their three lines of defense to properly perform their oversight function.

Figure 2: The three lines of defense in risk governance

– 1st line: Portfolio managers who “own” and manage the risks should be subject to effective management control. For example, the Head of Portfolio Management should be responsible for implementing corrective actions if necessary and to address control deficiencies.

– 2nd line: Risk management and compliance help building and monitoring the first line of defense controls. The risk manager monitors the portfolio versus the risk guidelines and supports the establishment of meaningful reporting. The compliance function monitors compliance with any applicable laws and regulations.

– 3rd line: Internal auditors are here to provide the senior management of the investment manager and the fund board with independent and objective assurance of the risk management and compliance procedures in place, i.e. the first two lines of defense. For example, aspects such as reliability of risk reporting, safeguarding of assets and compliance with contracts should be covered here.

Please do not hesitate to contact us to discuss your governance requirements.